If you've been working for 30 or 40 years, you've probably wondered when the right time is to retire and start collecting Social Security. The short answer is that it depends on your health, your savings, and how long you expect to live — but the trade-offs between claiming at 62, 67, and 70 are worth understanding before you make the call.

Here's how the three main options break down.

Claiming at 62 — the earliest you can start

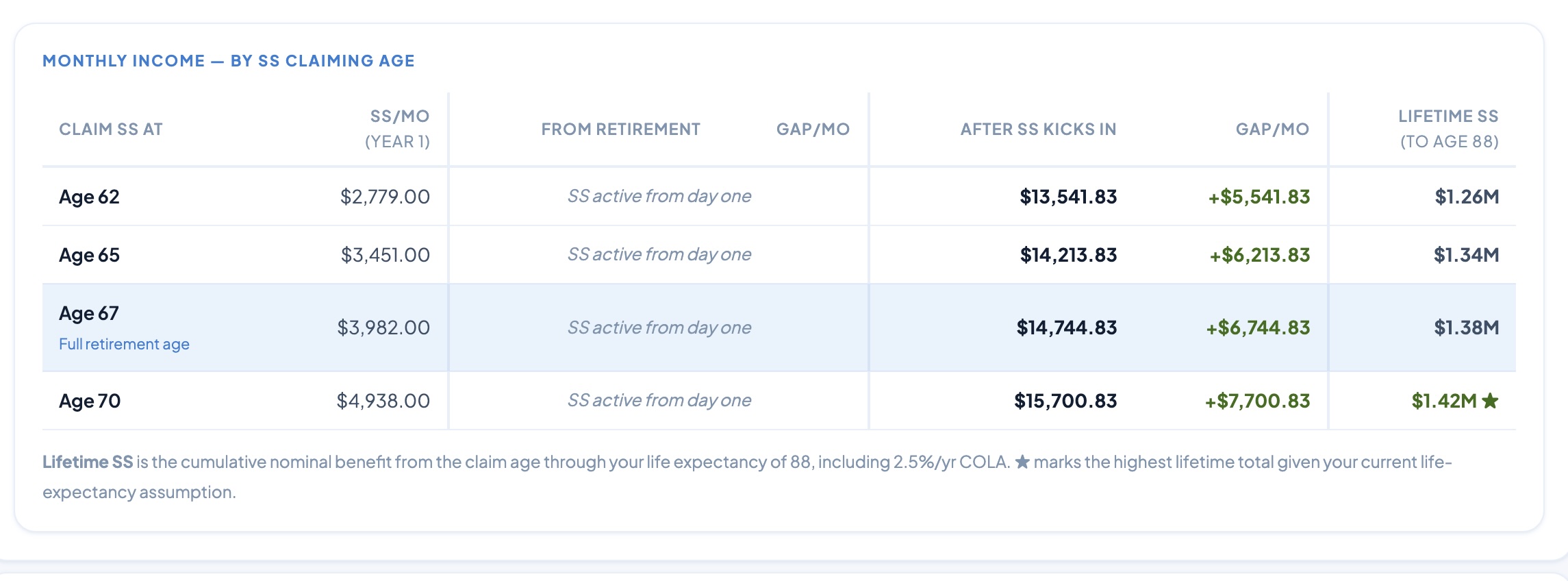

Age 62 is the earliest you can start collecting Social Security retirement benefits. The catch is that your monthly check gets permanently reduced — typically by about 30% compared to what you'd get at your full retirement age. That reduction doesn't go away when you turn 67. It sticks with you for the rest of your life.

There are still good reasons to claim early. If your health isn't great, if you've already stopped working and need the income, or if you have a shorter life expectancy in your family history, taking the smaller check sooner can be the right call. You also start collecting five years earlier, which means five years of payments the person waiting until 67 doesn't get.

One thing to watch: if you claim at 62 and keep working, Social Security will withhold some of your benefits if you earn over a certain amount each year. That earnings limit goes away once you hit full retirement age, but until then it can eat into the check you were counting on.

Claiming at 67 — your full retirement age

For most people retiring today, 67 is the full retirement age — the point where you collect 100% of the benefit Social Security calculated for you based on your earnings history. No reduction, no bonus. It's the baseline number on your Social Security statement.

Waiting from 62 to 67 means giving up five years of checks in exchange for a check that's roughly 43% larger every month for the rest of your life. Whether that math works out in your favor depends largely on how long you live. The break-even point is usually somewhere in your late 70s — meaning if you live past that age, you come out ahead by having waited.

The earnings limit also disappears at full retirement age, so if you want to keep working part-time without your benefits getting docked, 67 is when that becomes possible.

Claiming at 70 — the maximum benefit

If you delay past full retirement age, Social Security adds about 8% per year to your benefit, up until age 70. After 70 there's no further increase, so there's no reason to wait any longer than that.

The result is a monthly check roughly 24% larger than what you'd get at 67, and about 77% larger than what you'd get at 62. That's a significant difference, and for someone in good health with longevity in the family, it can be the highest-value choice. It also acts as a kind of insurance against living a long time — the longer you live, the more that bigger check pays off.

The trade-off is real though. You're giving up eight years of payments between 62 and 70, and you need enough savings or other income to bridge that gap. For some people that's not possible. For others it's the smartest move they can make.

Your numbers matter most

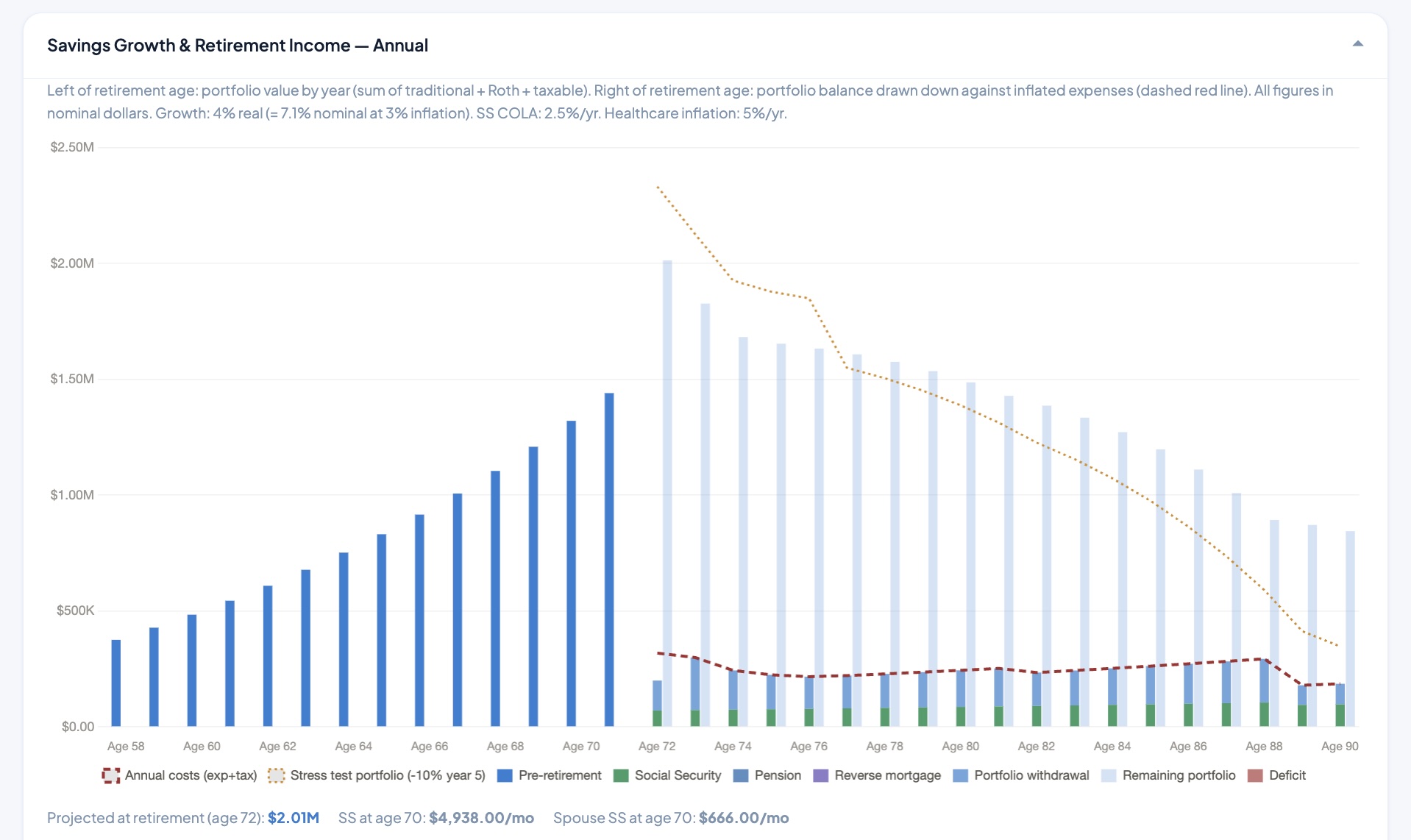

The decision isn't really about which age has the biggest check — it's about which age leaves you with the most money over your actual lifetime, given your savings, your spending, your other income, and how long you live. That's a calculation with a lot of moving parts, and rules of thumb only get you so far.

This is exactly the kind of thing my MyFinances app at myfinances.online is built to help with. You enter your portfolio, your expected expenses, and your Social Security estimates, and it forecasts what your finances look like under each of the three claiming ages. You can see side-by-side how your portfolio holds up if you claim at 62 versus 67 versus 70, including how long your savings last and what your total income looks like at different ages.

Seeing the actual numbers for your situation is a lot more useful than reading general advice about averages. The right answer for your neighbor isn't necessarily the right answer for you, and the only way to know is to run your own numbers.

Leave a comment